Economic Growth Looks More Resilient, Pushing Rate Cut Hopes Further Out

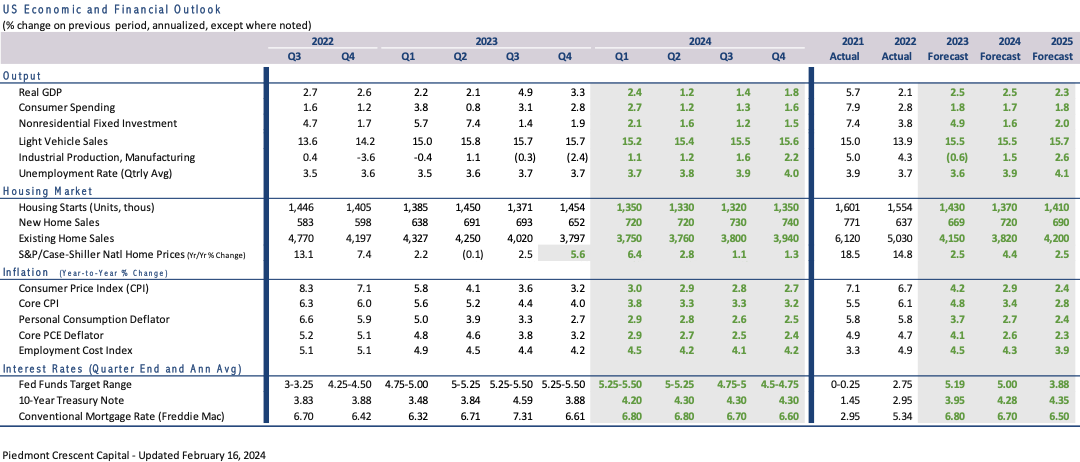

- January’s astonishing 356,000-job rise in nonfarm employment and upward revisions to prior months’ data suggest the economy began the year with surprisingly strong momentum. Consensus forecasts for first quarter GDP growth have been ramped up and remain above 2%, even following disappointing reports on retail sales and industrial production. Our own forecast calls for real GDP to rise at 2.4% in Q1 and 2.5% for all of 2024 (annual basis).

- A larger than expected rise in the January’s Consumer Price Index was the most disruptive data point this past month. The slightly larger than expected increase in both the headline and core price measures indicates inflation will not likely moderate as fast as the markets had expected. Broader price measures, such as the Cleveland Fed’s Median CPI, show that inflation remains sticky in many labor-intensive parts of the economy. The PPI data also came in on the high side.

- Higher and stickier inflation throws a wrench into the mechanics of forecasts calling for aggressive cuts in the federal funds rate this year. If inflation remains higher, real rates will rise less and likely limit the Fed to 3 or, at most, 4 quarter-point cuts this year, beginning in May or June. That trajectory is in line with the recent 2-Year Treasury yield, which consistently provides a good approximation of the federal funds rate one year out.

- While the U.S. economy is proving resilient, global economic growth is surprisingly weak. Concerted efforts by manufacturers to diversify their production base and supply chains continues to weigh on China’s economy. Japan and the U.K. have both fallen into recession. The US, India, and Mexico are notable upside surprises and offset part of this weakness.

- Weaker global growth should help curb inflation, giving the Fed room to cut rates. Geopolitical risks are boosting shipping costs, however, adding to global uncertainty. While the U.S. economy has repeatedly proved resilient, the business cycle appears both old and delicate in some respects, while vibrant and dynamic in others. Notably, the stock market's strength, driven by the AI revolution, mirrors the mid-1990s technology boom, producing a then record-long expansion.

Early data for the first quarter show the economy had strong momentum headed into the new year. Most notably, employers added 356,000 net new jobs in January and job gains for preceding months were revised higher. The gains were a bit of a surprise, as the annual benchmark revisions released with January’s data lowered the level of employment for the March 2023 benchmark month by 266,000 jobs. Hiring bounced back in the second half of the year, however, and ended the year slightly higher than previously reported under the 2022 benchmark. With the revisions, average monthly job growth for 2023 was revised up to 255,000 from 225,000 previously.

The upward revisions to the second half of the year’s jobs data are extremely unusual. Typically, revisions to subsequent months’ job growth follow the direction of the benchmark revisions, which were about 0.2% lower. While data for most months were revised slightly lower, data for December was revised up sharply, more than making up for the slight downward revisions. While unusual, the stronger job gains are consistent with stronger GDP growth during the second half of the year, which averaged a whopping 4.1% pace. The breadth of employment growth also improved toward the end of the year and in January.

How much weight should be assigned to January’s stronger employment data remains unclear. Nonfarm employment growth has averaged a 289,000-job pace over the past three months, much of which was due to a surge in job growth in December (333,000) and January (353,000). By comparison, employment growth in the prior year averaged just 244,000 jobs per month.

Employment is unusually volatile around yearend, with holiday hiring at retailers, restaurants, and delivery services spiking in November and December and typically plummeting in January. Seasonal adjustment smoothed these swings but the pandemic and changes in consumer behavior afterward have distorted this process. Just how large these seasonal factors are cannot be exaggerated. On a non-seasonally adjusted basis, employers cut 2,635,000 jobs in January. Since this was fewer job losses than usual, the seasonally adjusted data reported a 353,000-job gain.

Average weekly hours declined in January, falling 0.2 to 34.1 hours, the lowest since the Pandemic. The drop was impacted by harsh weather during the survey week. After leaping to 4.2% following the ISM manufacturing and construction spending reports, the closely watched Atlanta Fed GDPNow forecast for first-quarter GDP growth settled in at 3.5% in the aftermath of the strong employment figures. This measure has since retreated to 2.5% as more economic data have been released, close to our own forecast of 2.4% growth.

Stronger employment growth also implies the stellar productivity data reported for the fourth quarter might be revised lower from their preliminary 3.2% pace reported. The preliminary data also show productivity for the nonfarm business sector rose 1.2% for the year, which should be impacted slightly less. With 1.2% productivity growth and 4.5% wage growth, the Consumer Price Index will have a tough time breaking significantly below the most recent 3.1% year-to-year increase. Indeed, prices have been sticky for about anything where labor makes up a large proportion of costs.

Wages appear to have risen sharply in January, when higher minimum wages took effect in 22 states. Grocery prices rose 0.4% in January but have risen a modest 1.4% this past year. Prices have surged by 21.1% over the past three years, however, four times the pace of the preceding three years! The increase over the past three years is equivalent to the cumulative rise in grocery store prices from 2008 to 2021.

President Biden addressed rising grocery prices in a TikTok message before the Super Bowl, blaming 'greedy' corporations for what he called Greenflation and Shrinkflation. Shrinkflation involves reducing package sizes while maintaining the same price. Lael Brainard from the White House National Economic Council echoed these concerns, emphasizing wider profit margins at grocery stores. We see the inflation problem as more genuine. Average hourly earnings for grocery store workers skyrocketed 18.3% over the past three years and consumers have pushed back at efficiency measures, such as self-checkout. The problem with inflation is one of too much money chasing too few goods. While product shortages have diminished, wages are sticky and grocery stores, which historically operate on paper thin profit margins, have little capacity to cut prices.

Restaurants are another area where higher wages are being passed along to customers. Restaurants have been short staffed since the economy emerged from the Pandemic, which has sent average hourly earnings soaring 31.7% over the past three years. Not surprisingly, prices are up substantially, making restaurant dining more of a luxury for about everyone. Sales at restaurants and bars were one of the bright spots in an otherwise dreary January retail sales report. Sales at restaurants rose 0.7% in January and are up 6.3% over the past year. After accounting for inflation, however, sales rose just 0.2% in January and are up just 1.2% over the past year.

We remain cautious about inflation. Pandemic-driven price swings, particularly for used cars, health care services, and apartments, skewed seasonal adjustments and understated inflation as prices stabilized in 2023. We expect inflation to remain firm through the middle of this year, as prices for health care services rebound during the second half of last year.

The Cleveland Fed’s Median CPI provides a more consistent assessment. Despite higher readings, this measure still suggests moderating prices, enabling the Fed to initiate a quarter-point cut in the federal funds rate by the end of June, followed by successive cuts in September and December. Our forecast is well below the market consensus, as shown by the CME’s fed funds futures but the aligns with the recent trend in the 2-Year Treasury Note, which has reliably provided an indication of where the federal funds rate will be one year ahead. Fed funds futures are continuing to look for five or six quarter-point cuts over the next year.

Let there be no doubt, the Fed is walking a fine line. Monetary policy is tight today, as can be seen by higher real interest rates. The effective federal funds rate is currently 5.33%, which is 213 basis points (bp) above the latest change in overall CPI and 143 bp over the core CPI. A neutral fed policy, with the economy at full employment, would peg the real federal funds rate at between 50 bp and 100 bp over the core CPI. The Fed would like to be able to lower interest rates, which might extend the business cycle and help avoid the problems in the commercial real estate sector from metastasizing into a systemic threat. The Fed does not want to ease too early or by too much, which would put its hard-won gains at bringing down inflation at risk.

We see the overall CPI easing to 2.7% by the end of 2024 and look for the core CPI to decelerate to 3.2%. That should provide the Fed with enough room to cut the funds rate three or four times by year-end. While our forecast still has three rate cuts in it, recent data show the global economy slowing more abruptly. China is now a source of global disinflation in goods, reflecting efforts to stem the exodus of firms looking to diversify their supply chains. Growth has also weakened in Japan and the UK – both of which are in recession. Weaker global growth may cause inflation to ease faster and might allow the Fed to ease a little sooner.

The Fed also must guard against further fueling asset bubbles. The stock market has rallied strongly ever since the December FOMC meeting when the Fed made it clear that they had finished raising interest rates. While the markets suffered a brief setback following January’s disappointing CPI report, the market quickly bounced back and handled the disappointing Producer Price Index data much better. Initial public offerings and mergers and acquisitions have also increased, as have share buyback announcements and even the venture capital market. All of which are good things in moderation but can lead to a massive hangover if they rise out of proportion with the underlying fundamentals.

Lower interest rates would surely benefit the housing sector. Many current homeowners secured ultra-low interest rates during the prolonged period of near-zero short-term rates during and immediately after the pandemic. Presently, around 78.7% of first-lien mortgages have rates of 5% or less, with 59.4% below 4% and 22.6% below 3%. With current mortgage rates hovering around 6.80%, homeowners are understandably hesitant to sell their homes, fearing significant increases in their housing cost even if they are downsizing. Consequently, there is a shortage of existing homes for sale, which has driven up prices and led to near-record lows in housing affordability.

The dearth of existing homes has been a godsend for home builders. Many potential home buyers that would have purchased an existing home are now looking to purchase a new home and home builders have ramped up their offerings of entry-level homes. Home builders are also offering financing incentives to reduce the sting of higher mortgage rates. The result is a two-tiered housing market. New home sales and single-family housing starts are holding up well, while existing home sales, which is a much larger market, continue to struggle.

Mortgage rates had pulled back prior to January’s surprising CPI report but have now surged back toward 7%. That earlier pullback in mortgage rates had boosted home buying but buyer traffic has slowed more recently. We expect mortgage rates to decline gradually this year and to end the year around 6.40%. Unfortunately, mortgage rates will have to drop well below 6% before a substantial number of existing homeowners will feel comfortable enough to part with their current low-rate mortgage and put their current home on the market.

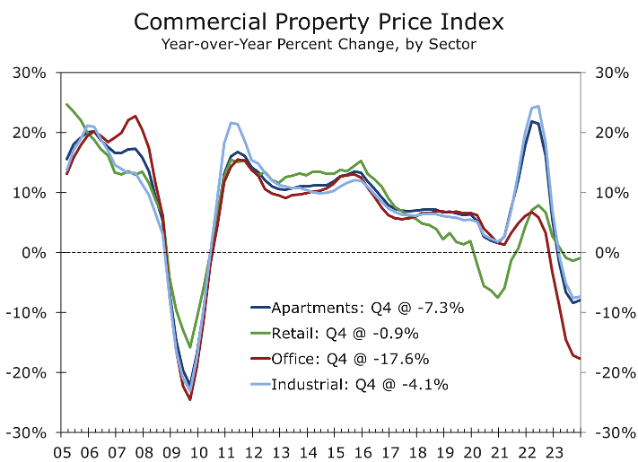

Lower interest rates would be even more beneficial in helping resolve the brewing troubles in commercial real estate. Real estate values are closely tied to interest rates, as the stream of rents earned from owning income producing properties is more valuable when interest rates are lower. Property values skyrocketed during the pandemic period and its immediate aftermath, when short-term interest rates were near zero and real estate investors who were overcommitted to gateway markets rushed into secondary markets in the Sun Belt. Apartments and industrial properties saw the largest increase. Prices for retail and office properties rose less.

Property price appreciation surged in late 2021 and early 2022, but then slowed sharply as the Fed raised interest rates more aggressively than anticipated. Office building prices, especially older ones in downtown areas, were significantly impacted. Concerns have arisen about a potential repeat of the Global Financial Crisis, but Fed and Administration officials, including Treasury Secretary Janet Yellen, do not foresee a systemic crisis threatening the banking system.

The problems in commercial real estate are both simple and complex. From a simple standpoint, commercial real estate values have come under pressure because interest rates have risen abruptly, while rents have risen less rapidly or fallen. Moreover, insurance and operating costs have risen substantially. Changes in consumer behavior in the aftermath of the pandemic introduce a more complex component into the outlook. One of the most obvious changes has been the slow return to the workplace, particularly in downtown areas, which has led many large employers to consolidate office space and sent values for some office buildings plummeting.

Not all office buildings are struggling, however, and office buildings are just one asset class within commercial real estate. Newer office buildings are performing relatively well, as employers are striving to entice workers back to the office. Many suburban properties are also faring better, as workers are more inclined to return to offices in the suburbs that are closer to home and do not charge for parking.

Commercial real estate looks far less menacing outside of the office market. There are a record number of apartments currently under construction, which will cause vacancy rates to rise later this year. But all these apartments will not be completed at once and there is an undersupply of housing in general. Nevertheless, property prices will fall this year and some investors may have trouble rolling over their maturing debt. Lower interest rates would make this easier.

Elsewhere, the industrial market and retail market are likely to see few problems. To be certain, property prices are correcting but demand remains strong. The industrial market is benefiting from reshoring and continued growth in online retailing. Both have much further to run. The retail market is also doing better. The sector has seen little construction this past decade and is seeing strong demand for open-air retail space. Flexible work schedules mean workers have more time to shop, travel and entertain, which is good for brick-and-mortar retail.

We have once again boosted our near-term forecast and see real GDP rising at a 2.4% annual rate during the first quarter. When taken together with the stronger growth in the second half of last year, real GDP is likely to grow 2.5% this year on an annual average basis, even though not one single quarter will see growth that high. On a fourth-quarter-to-fourth-quarter basis, we look for real GDP to rise 1.7% in 2024.

Inflation is expected to continue to moderate, although labor-intensive services will continue to see larger price gains. Shipping delays due to the attacks in the Red Sea and low water levels in the Panama Canal have also boosted container rates, which presents some near-term risk. We look for a more meaningful deceleration in inflation in the second half of this year, which should allow the Fed to gradually reduce the federal funds rate.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable. © 2023 CAVU Securities, LLC

Questions? Email: CompassReport@cavusecurities.com