![]()

Plotting a Course Back to the New Normal

- Attention remains keenly focused on the Federal Reserve’s plans to begin to reverse the tightening they put in place a couple of years ago after they realized inflation would prove more persistent. The financial markets now look for the Fed to begin cutting the federal funds rate no sooner than June and look for a total of three quarter-point cuts this year – a view the Fed affirmed at its March 20 FOMC meeting.

- The slower consensus view on rate cuts follows a series of stronger monthly employment reports and hotter inflation reports. Job growth is simply too strong, and inflation is too high to allow rate cuts any earlier than June. Most other economic reports paint a softer economic portrait, with retail sales and industrial production remaining weak, consumer confidence remaining guarded, and survey of consumers and businesses continuing to show inflation and wages moderating.

- The Federal Reserve is currently tracking multiple objectives. The principal target is long-term price stability, which means returning core inflation measures back to a 2% pace. The second is maintaining full employment, which means keeping the unemployment rate around 4% and maintaining high levels of labor force participation. A third objective is to avoid surprises and policy missteps, particularly ones that would lead to financial volatility. The Fed’s final objective is to accomplish all of this without becoming a political issue in this year’s election.

- While the Fed’s objectives are straightforward, their timetable remains fluid and is ongoing. The recent obsession with the latest employment and inflation numbers misses this point, as the Fed is looking more at where the economy is headed rather than where it has been or currently is. Monetary policy works with a long and variable lag, so the Fed’s moves must be taken before employment slows too much and well before inflation has returned to target.

- We have made some slight adjustments to our forecast and see economic growth moderating this spring and summer. The Fed is expected to cut the federal funds rate by a quarter percentage point in June and follow that with cuts in September and December. We expect additional cuts in 2024 but do not believe the Fed is in any hurry to bring the federal funds rate back to neutral.

The March Federal Open Market Committee (FOMC) meeting marked a seminal event for many forecasters and market participants. While the Fed was widely expected to leave the federal funds rate unchanged, attention was keenly focused on any adjustments made to the forecast for economic growth, inflation, and interest rates. Back-to-back strong employment reports raised expectations for growth this year, while the first two rounds of inflation reports showed inflation would likely prove sticky this year and take long to return to the Fed’s 2% long range target. Most other economic data have been mixed, with retail sales beginning the year on a weak note and industrial production and most survey data suggesting economic growth is slowing.

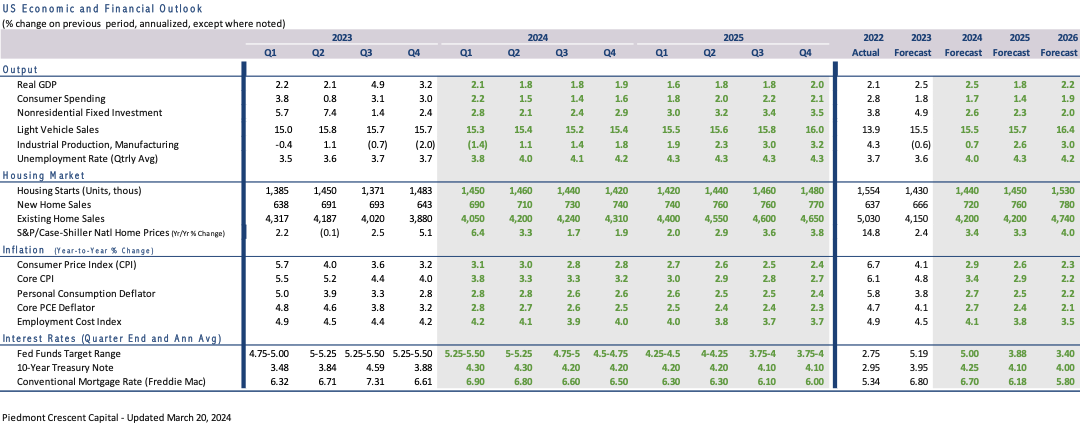

For its part, the Fed raised its estimate for economic and now expects real GDP to rise 2.4% from the end of 2023 to the end of 2024, versus 1.4% previously, and rise 2% in both 2025 and 2026. The unemployment rate is expected to remain close to 4%, while inflation, as measure by the core PCE deflator, is expected to gradually decelerate to 2.6% this year and 2.4% in 2025, before finally returning to the Fed’s long-run target of 2% in 2026. The Fed continues to expect three quarter-point rate cuts in 2024, followed by three more in both 2025 and 2026, bringing the federal funds rate down a cumulative 225 basis points to 3.125% by the end of 2026.

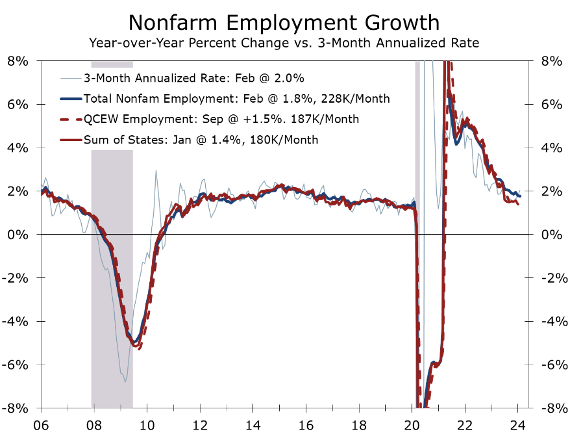

To paraphrase Yogi Berra, it’s tough to make predictions, especially about the future - even if you are the Federal Reserve. The Fed’s stronger economic forecast is consistent with the stronger employment data reported for the past three months. Private and public employers have added an average of 265,000 jobs a month for the past three months and an average of 229,000 per month over the past year. Our research suggest the currently reported employment data overstate nonfarm employment by approximately 800,000 jobs, however, and peg monthly job growth over the past year at just 175,000 jobs per month. We expect to see a moderation in reported job growth this spring, aligning more closely with the recently released Quarterly Census of Employment and Wages, as well as the revised state and local employment data.

Slower job growth would make the Fed’s job easier, particularly if the inflation data continue to come in hotter than expected over the next few months. The one change in the Fed’s policy statement following the March FOMC meeting was to acknowledge the strong job growth reported over the past three months, noting that “job gains had remained strong”. This is a slight upgrade from prior meetings. While the Fed sees job growth remaining strong, they also see the labor market moving back into balance, with job openings and the quit rate both declining, which is a precursor to a further moderation in wage gains.

If job growth slows along the lines we expect, the Fed will more easily be able to justify cutting interest rates, even if inflation continues to prove resilient. Seasonal adjustment issues likely understated core inflation during the second half of 2023 and the payback is now boosting it. The Fed left themselves a little more room on this front by slightly lifting their expectation for core PCE inflation to 2.6% this year from 2.4%.

Source: Bureau of Labor Statistics

The Fed’s stronger economic outlook and more cautious view on inflation not only match up well with recent economic reports but also provide them with a great level of flexibility, which they very well may need. The Fed operates with multiple objectives, primarily centered on achieving long-term price stability with a 2% inflation target while simultaneously striving to maintain full employment, defined by a roughly 4% unemployment rate. The primary tool used to accomplish the Fed’s goals is raising or lowering the federal funds, which they strive to do in a way that avoids policy missteps, prevents financial volatility, and remains apolitical, particularly during election cycles.

The Fed’s strategy and tactics change over time, reflecting both short-term cyclical and long-run structural influences. The Fed aggressively slashed interest rates at the onset of the pandemic, reduced interest rates to zero and substantially expanded its balance sheet to bolster liquidity to the broader economy and financial markets and also accommodate the surge in federal spending. This extraordinarily accommodative stance persisted until early 2022, when mounting inflation pressures emerged due to the economy's reopening amid widespread supply chain disruptions and bottlenecks.

After recognizing that the threat from inflation was considerably more extensive than just shortages and bottlenecks, the Fed ramped up the pace and magnitude of their rate hikes, including hiking the federal funds rate by 75 basis at four successive meetings back in summer and fall of 2022 before tamping down the pace of rate hikes this past year. At the December FOMC meeting, the Fed said that it had likely finished hiking interest rates for this cycle, which turned attention to the prospect of rate cuts in 2024. At first, market expectations had priced in six rate cuts for this year. Expectations for rate cuts have been scaled back more recently, following back-to-back stronger-than-expected employment reports and hotter-than-expected inflation reports.

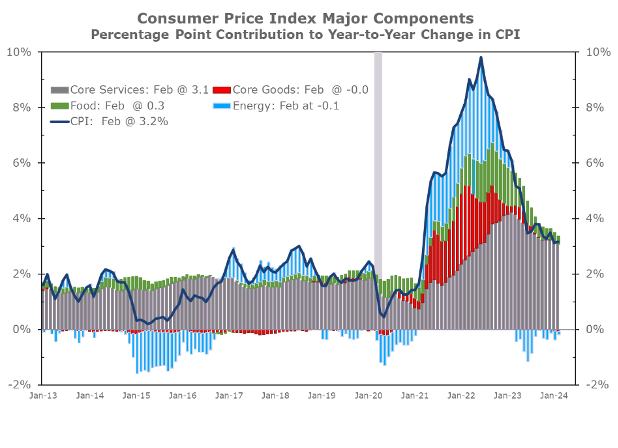

While inflation has remained more persistent than expected, it has slowed considerably since the Fed became more aggressive about hiking interest rates. The year-to-year change in the Consumer Price Index peaked out at 9.1% in June 2022 to just 3.2% in February of this year. Most of that improvement came from falling energy prices. Prices for used cars and SUVs also reversed much of the spike seen during the pandemic and food prices, which had risen sharply in 2021 and 2022, rose less rapidly this past year. Core services prices, which account for the bulk of consumer outlays, have moderated much less and now account for the bulk of overall inflation.

Source: Bureau of Labor Statistics

We remain cautious regarding inflation, especially given the pandemic's impact on price fluctuations. Certain sectors such as used cars, health care services, and apartments experienced significant price swings, which likely distorted seasonal adjustments and led to underestimated inflation, particularly in the latter half of last year despite a general moderation in overall price increases. Looking ahead, we anticipate inflation to remain elevated until the middle of this year, particularly as prices for health care services rebound from their previously understated levels towards the end of last year. Additionally, energy prices are on the rise once again, with crude oil recently surpassing $80 a barrel and national retail gasoline prices recently topping $3.50 per gallon, according to AAA.

Core services prices continue to pose the primary challenge to reducing overall inflation. Excluding energy, services prices increased by 5.2% over the past year, with core services inflation reaching a peak of 7.2% in February 2023 and decelerating less than overall core inflation since then. Housing costs, particularly owner’s equivalent rent and residential rent, have been significant areas of concern, as they have slowed less compared to many widely followed private rent indices. These indices predominantly sample asking rates on professionally managed apartments and single-family rental homes, whereas rents for lease renewals have shown greater resilience. With 450,000 new rental apartments expected to enter the market this year, residential rents will likely moderate further and this moderation should show up more clearly in the government inflation data.

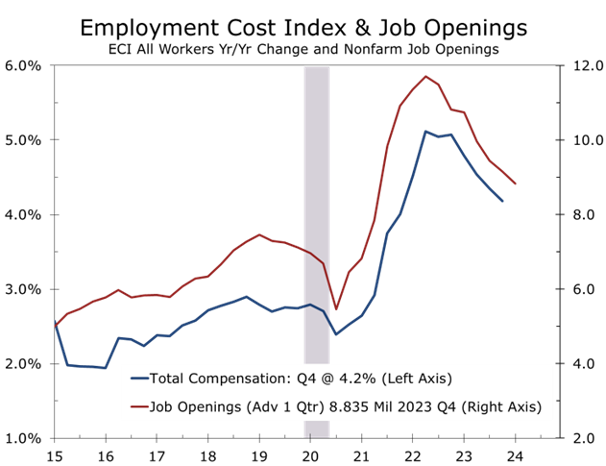

Core services inflation, excluding housing, remains problematic, surging 0.9% in January and rising 0.5% in February. Auto insurance and car repair have been a major part of the problem but prices are up sharply in almost every industry where labor makes up a large proportion of costs. The focus on core services prices brings attention back on the labor market, where the number of job openings has cooled off considerably over the past 18 months. There is a pretty tight relationship between job openings and the Employment Cost Index (ECI), which is a broader measure of labor costs that includes benefits. We expect job openings to recede further this year, although the rate of deceleration is expected to slow somewhat. Much of the recent strength in job growth has been at state and local governments, health care, and the leisure hospitality sector, which are all striving to bring hiring back in line with its pre-pandemic trend.

Source: Bureau of Labor Statistics

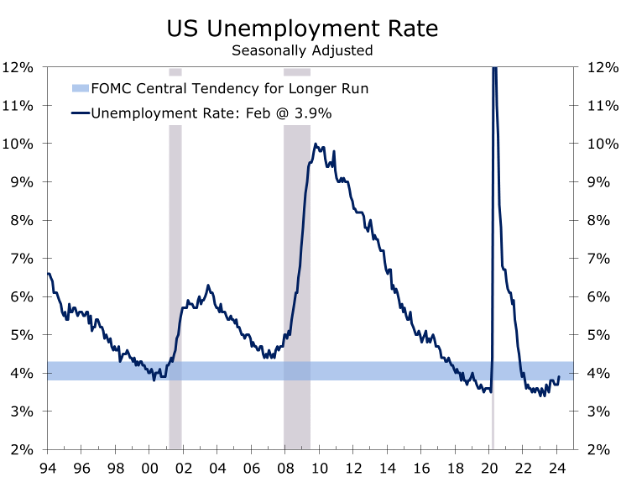

Another sign that the labor is moving back into balance is that the unemployment rate has edged higher in recent months, climbing to 3.9% in February. With the latest rise, the unemployment rate is back within the Fed’s long-run target range of between 3.8% and 4.3%. The rise in unemployment results from slower household employment and slightly stronger labor force growth. The household employment measure is notoriously volatile around the turn of each year when there is significant movement into and out of the labor force and the Labor Department also makes their annual population adjustment.

How much should be made of the recent uptick in the unemployment rate remains to be seen. An increase in the unemployment rate of half a percentage point or more has typically marked the start of a recession. The jobless rate is now up 0.5 percentage points from its low hit in April of last year and is 0.2 pp above its average for the past year. Why this rule would hold any more sway in the post-pandemic environment than the inverted yield curve or nearly two-year slide in the Leading Economic Index is certainly a key point to consider. A better counterpoint, however, is weekly unemployment claims remain at 50-year lows and there are still more job openings than there are unemployed. Consumer surveys also show relatively little concern about job security.

We suspect the rise in the unemployment rate reflects a host of factors. Part of the increase is purely cyclical. Manufacturing has endured a slowdown this past year, which has seen industrial production decline 0.8% over the past year and manufacturing employment has been essentially flat for the past year. Hiring has also slowed in construction, reflecting a winding down of some commercial projects and some slowing in industrial projects. Much of the strength in hiring has been in government, health care, and the leisure and hospitality sector.

Structural factors may also be pushing the unemployment rate higher. There was a surge of immigration in 2023, which likely pushed labor force growth higher and resulted in a slightly higher unemployment rate when hiring slowed during the second half of last year. We look for the unemployment rate to continue to edge higher this year, rising to 4.2%, where we expect it to remain through much of next year. From a longer-term perspective, the jobless rate should remain relatively low, as a growing number of Baby Boomers continue to retire and exit the workforce. The last Baby Boomer will turn 65 in 2029.

Source: Bureau of Labor Statistics

Stronger immigration is one of the reasons the Federal Reserve raised their forecast for economic growth this year. The Congressional Budget Office estimates that immigration, including undocumented individuals, surged to 3.3 million in 2023, which is well above its pre-pandemic pace and roughly 2.3 million ahead of the CBO’s estimate for 2023 made back in 2019. While political factors will likely slow immigration this year, we still expect a net gain of at least 2.3 million residents, which will bolster labor growth and potential GDP.

Domestic factors will also bolster economic growth, with household formation and live births both expected to increase this year. The increase in household formations continues to be driven by younger households, which is one reason apartment demand has remained so strong. Apartment vacancy rates are expected to increase this year, however, as just over 450,000 apartments are expected to be completed, primarily in the South and Mountain West. Millennials are also increasingly forming families and having children, which is driving demand for starter homes.

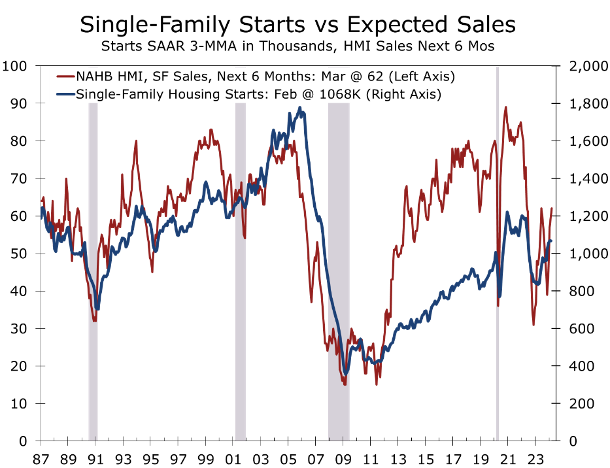

Home building is expected to be a significant driver of economic growth this year. Mortgage rates are projected to decline, with the rate for a 30-year conventional mortgage expect to fall to 6.50% by the end of the year. Home builders are extensively utilizing mortgage rate buydowns, resulting in a steady rise in buyer traffic. The NAHB/Wells Fargo National Housing Market Index (HMI) climbed 3 points in March to 51, marking its fourth consecutive increase and reaching its highest level since July of last year. Builder expectations for sales over the next 6 months also rose by 2 points to 62, matching their highest level in 21 months.

The rise in home builder optimism is apparent in the latest housing starts, which surged by 10.7% to a pace of 1.52 million units in February. Single-family starts rose by 11.6% to a 1.13 million unit pace, are up 35.3% from last February. Multifamily starts, primarily rental apartments, rebounded by 8.3% in February to a 392,000 unit pace, following a 27.9% decline the previous month. Despite this rebound, multifamily starts remain 35% below their year ago pace. The rise in single-family starts is expected to have positive ripple effects, as an increasing number of new home sales are from first-time buyers who will require financing, insurance, and furnishings for their homes. This will boost financial services and the production and sales of furniture, household appliances, home furnishings, and building materials used in home construction.

Source: Census Bureau

We have extended our forecast out through 2025 on a quarterly basis and 2026 on an annual basis. Current quarter real GDP growth is estimated at 2.1%, fueled by strong growth in consumer spending and stronger sales of both new and existing homes. Business fixed investment also looks solid, although we are seeing a growing number of Electric Vehicle-related projects postponed. Growth is expected to moderated this spring and summer to just under a 2% annual rate. Our forecast for the year calls for real GDP to rise at a 2.5% annual rate on an annual basis and 1.9% pace on a Q4-to-Q4 basis, slightly below the Fed’s 2.1% projection.

There has been a great deal of discussion following the March FOMC meeting regarding the decision to raise both the growth and core inflation forecast but keep plans for a June rate cut in place. The return to the Fed’s 2% target is more likely to reflect a long and winding road rather than straightway. Chair Powell acknowledged as much in his press conference. We expect to see this debate heat up following what we believe will be disappointing inflation numbers next month. The inflation data should look better this spring, however, and we feel confident they will cut in June and September and then wait until after the presidential election to cut a third time. Inflation is not expected to return to a 2% pace on a sustained basis until 2026.

We see some upside risks to our forecast. The most cyclical parts of the economy appear to be regaining momentum. Early reads on manufacturing activity in March show an improvement in orders, output and shipments. Construction activity also appears to be ramping up, with single-family starts up 35% from their year ago levels. New home sales are expected to rise 8% this year and existing home sales are expected to rise at least 1% to a 4.2 million unit pace. The risk is to the high side, however, as a growing number of homeowners are putting their homes on the market. The resulting knock-on effects will lift economic growth more broadly.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

Questions? Email: CompassReport@cavusecurities.com